The IFT responds to Part 26A Practice Statement Consultation

The IFT submitted a response last week on the replacement Practice Statement covering Part 26A Restructuring Plans, which welcomed the...

Insights and reports

Share this

David Tilston, listed company CFO and IFT member, shares his insights on a liquidity key lesson at times of crisis: build a rolling cashflow.

I have dealt with a number of liquidity situations in the past, ranging from the severe to the potentially terminal. I pass on one useful lesson I have learnt.

The lesson

Get a 13 week rolling cashflow forecast started as soon as possible, ideally this week, and update it weekly.

What is a 13 week rolling cashflow forecast?

It is a forecast which starts from a confirmed cash position (normally at the end of the prior week) and forecasts your cash balance at the end of each of the next 13 weeks. It is based on explicit assumptions around the cash receipts (normally from customers) you expect to receive, and the cash payments (including salaries, supplier invoices) you expect to make.

Why is it important?

It gives you a forward looking view as to your liquidity and whether you are in danger of running out of cash in the short term. If you are, then at least you can see when and decide what actions you need to take.

If you want to seek help from your lenders then you will be asked to produce a 13 week rolling cashflow forecast, and they may ask an external firm to review it. If you cannot produce such a forecast, then your lenders will have less confidence in the company being able to manage its liquidity position. In addition, it will give the lenders some perspective on how quickly they need to act and the potential amounts they might need to lend in the short term (possibly whilst a longer term solution is being worked on). If you are asking the lender to put in a large amount of cash next week, they may withdraw their support. The longer the notice period to the lenders, the more opportunity they have to potentially be supportive.

Some typical responses and how to deal with them

“We do not have time to do this” – It is much better to have a blunt forward-looking view of cashflows rather than a detailed backwards-looking analysis of performance, as the latter does not help you take the requisite cash preservation decisions in time. If you are not forecasting cashflows then you are not going to see with clarity an emerging problem which may be approaching rapidly, and this will not be good for credibility with your lenders should you have to speak to them.

“The forecast will be wrong” – this is absolutely correct as some assumptions and all forecasts will be wrong. However, the more you do it the better you will get at it.

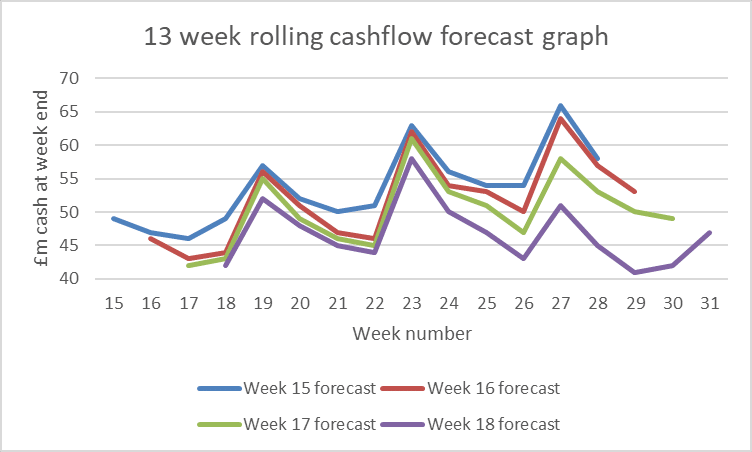

“Why do I need to update it weekly?” – Firstly, so you can reconcile your week 1 forecast to the actual outturn 7 days later and understand where your forecasts were wrong (and therefore how to improve them). Secondly, you want to understand how your forecasts are evolving over time, and this is most easily done by graphing several of the forecasts on a weekly basis (as shown in the graph below). If the forecasts are generally consistent over a number of weeks and you project closing cash balances within a reasonable tolerance, then you can have greater confidence in your forecasting ability. If forecasts are continually ahead of reality and being downgraded (as shown in the graph) then that is probably a warning sign your assumptions are too optimistic.

“Why do I need to start this week?” – it typically takes a few weeks for the forecasting disciplines to settle down as staff learn the process and get feedback from weekly reviews, so the earlier you start the sooner you will have greater reliability.

It is much better to have a blunt forward-looking view of cashflows rather than a detailed backwards-looking analysis of performance

Some tips:

This is not something the finance function can do on its own, and it will need to actively engage with a number of other functions such as purchasing, manufacturing and sales. It is important that those imputing assumptions to the finance team understand why they are being asked and what the impact is from a cash perspective.

The forecast needs to be properly internally reviewed weekly along with a variance analysis to the forecast produced the week before, particularly for the first week of the forecast to the actual outturn (i.e. on Monday we forecast having £5m of cash at the end of the week but we only had £4m – why?). This will generate a feedback loop which helps to improve the accuracy of the forecasts.

The various functions may produce assumptions which are internally inconsistent (for example manufacturing is producing twice as much as the sales team think they can sell). This is not unusual, and the process of agreeing integrated and consistent assumptions between the various functions should improve the outlook for the business.

Depending on your commercial dynamics (for example the retail sector will behave quite differently to the manufacturing sector) nearer term projections are likely to be more accurate than longer term ones. The first 4 weeks may be reasonably accurate as the assumptions used will largely be driven by debtors and creditors already included on the balance sheet. Weeks 5-8 should be informed by customer and supplier conversations which are taking place currently where transactions are shortly to be agreed. The forecasts for weeks 9-13 are likely to be more volatile as the assumptions to be used may be less clear. Do not worry – this is quite normal – but the forecasts should still be completed.

There may be relatively junior staff who can be incredibly valuable. I have found on more than one occasion that I have a cashier in the finance function who really understands many of the cashflows and has an intuitive “feel” for them. These individuals need to be encouraged to speak up as their input may be disproportionately valuable to the business.

Conclusion

This is not a comprehensive analysis of liquidity issues, simply my own most important lesson from past crises. So I say again:

Get a 13 week rolling cashflow forecast started as soon as possible, ideally this week, and update it weekly.

Members of The IFT saved an estimated 56,000 jobs in 2023-24.

IFT members helped add £3.1 billion in shareholder value in 2023-24.

Over 80% of IFT members reported being busier or as busy 2023-24 compared to the previous year.

Over 60% of stressed companies don’t know they are in trouble until it is too late.

The IFT submitted a response last week on the replacement Practice Statement covering Part 26A Restructuring Plans, which welcomed the...

You can read our Q2 edition of Swift here. This includes summaries of sessions at our recent regional conferences, as...

The IFT’s latest quarterly snapshot for Q1 2025 showed a mixed picture for turnaround and restructuring activity in the quarter: ...

As we move through 2025, the mantra of the UK government continues to be focused on growth, growth, growth. In...